Inflation rates today are topping 10% or more in some countries and putting pressure on consumer spending in ways not seen since the 1970s. Many consumers are cutting back on subscription services to economize during the cost-of-living crisis.

Earlier this year, for example, Kantar found that over one million music streaming subscriptions in Great Britain had been cancelled in Q1 2022. Thirty-seven percent of respondents cited the desire to save money as the main reason.

Kantar surveyed US consumer uptake of a broader range of subscription services in April 2022 and again in August 2022. We explored how gender, age, and income levels correspond to the number and type of subscription services that people have across eleven categories, including streaming services, broadband, food and meal kits, insurance, clothing, cosmetics, and personal care.

We also looked at how age and income cohorts differ with respect to:

- The number of subscriptions held in different categories

- How many subscriptions each would cancel if allowed

- How closely each monitors subscription expenditures

- How each responded when last asked to renew the service

- How diligent each is at claiming refunds and benefits

Here’s what we found.

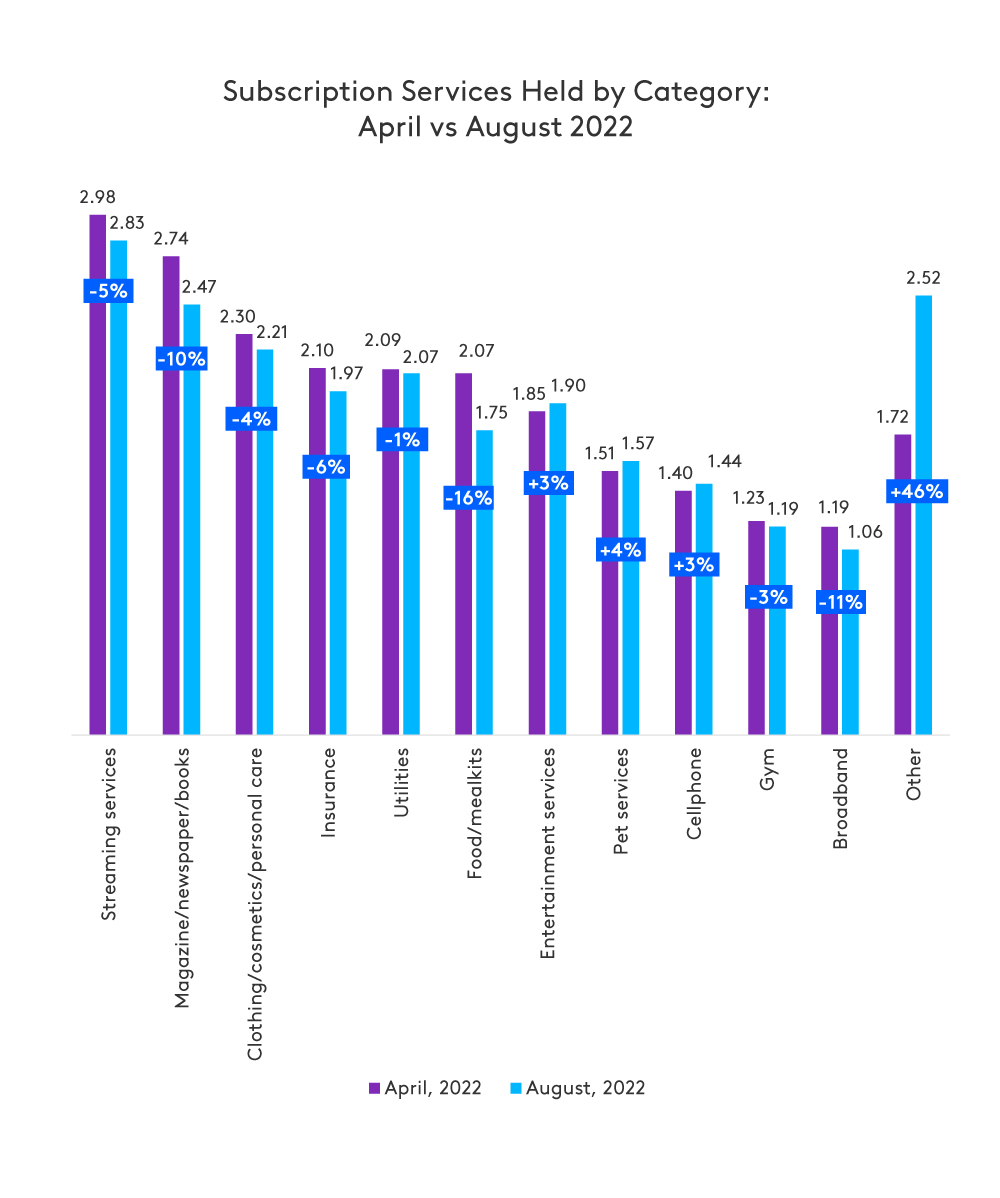

No significant growth in subscription services

The average number of subscriptions to entertainment services, pet services, and cell phones showed very slight increases from April to August 2022. Average subscription levels fell across eight other specific categories in this timeframe.

These results suggest that the cost-of-living crisis may be causing people to economize by either cutting back on subscriptions or not taking on new ones. As it is too early to tell how a longer inflationary or recessionary cycle might affect customer enrolment in subscription services, Kantar will look to monitor this important segment of household spending.

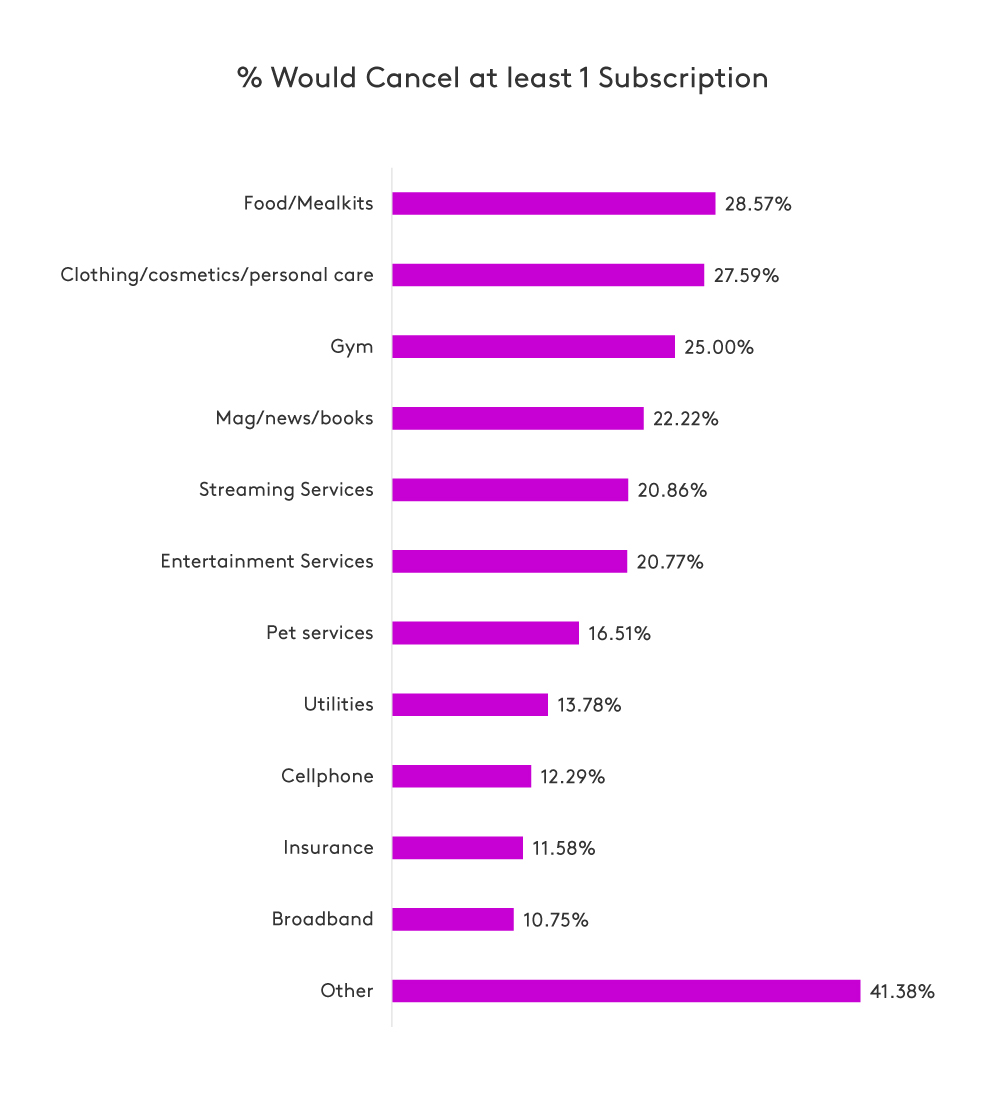

Desire to cancel subscriptions varies by type of service

Approximately 1 of 4 respondents would cancel at least one of the following; gym subscription (25%), food or meal kit (29%), or clothing/cosmetics/personal care subscription (28%) if given an opportunity to do so.

Though broadband has relatively low uptake versus other specific subscription categories, it has the lowest percentage of respondents who would cancel (11%). Perhaps broadband is deemed as a necessity and not a luxury.

Approximately 1 of 5 respondents would like to cancel at least one of the following: streaming services (21%), entertainment (21%), and magazines/newspapers/books (22%).

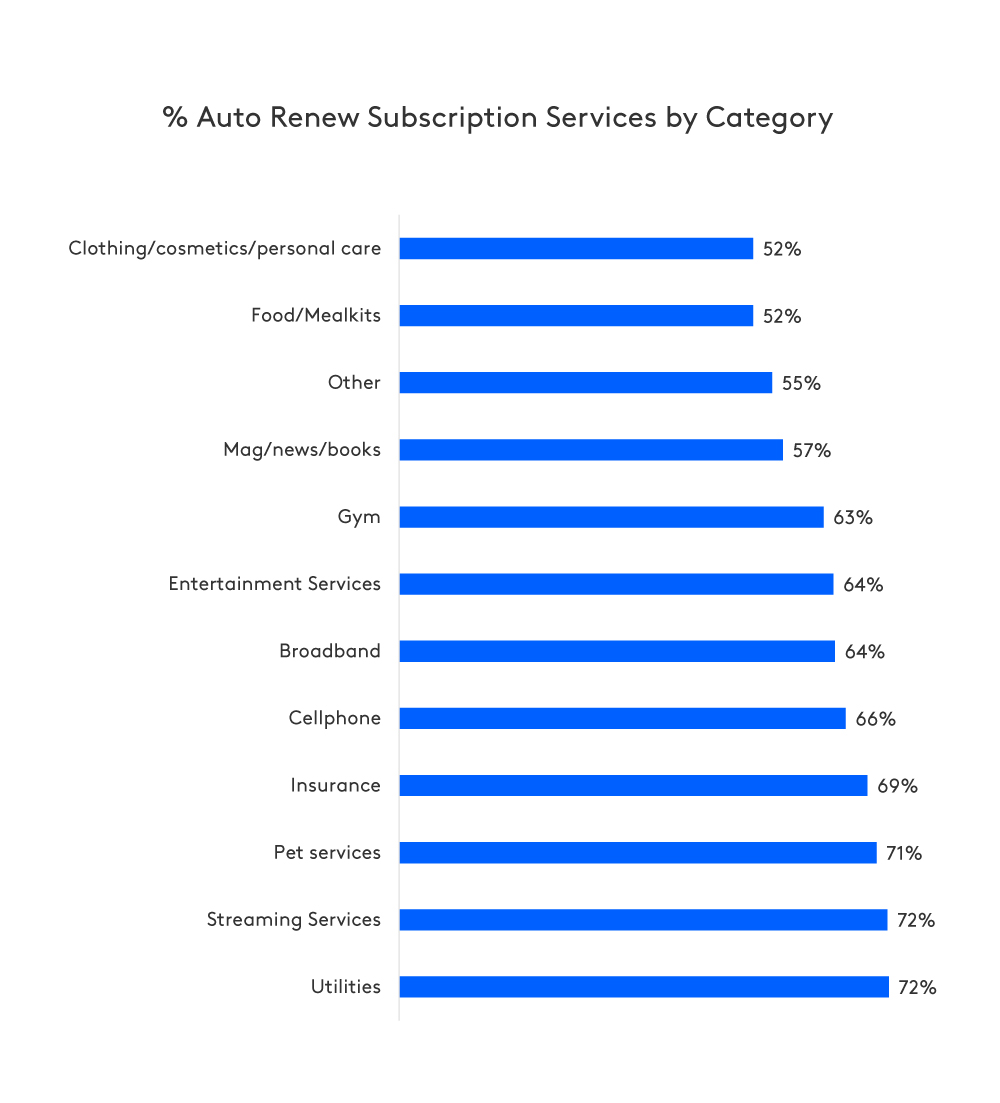

Auto-renewal is a powerful tool

When it comes to making a decision about keeping a subscription, auto-renewal dominates all other options available to consumers.

Streaming services and utilities have the highest number of auto-renewals (72%), followed closely by pet services (71%), and insurance (69%).

Food and meal kits, as well as clothing/cosmetics/personal care subscriptions, have the lowest rate of auto-renewal (52%). These two categories also show identical results across the remaining options. Thirteen percent of respondents would ask for a better deal in both cases, while 12% would opt to find a better deal elsewhere, and 12% decide to cancel before renewal.

Following auto-renewal, consumers are most likely to ask for a better deal for entertainment services (18%) and broadband (17%).

The most, and least, popular services are the same in April and August

In August 2022, consumers averaged 1.94 total subscriptions (inclusive of all categories), compared to an average of 2 subscriptions in April.

The top three most popular subscription services (total) by category were the same in each survey. Streaming services ranked first, followed by magazines/newspapers/books in second place and clothing/cosmetics/personal care in third. In all three cases, the average number of subscriptions declined slightly between April and August.

The three least subscribed categories were also consistent. In descending order, pet services ranked ninth, gym services tenth, and broadband last in both surveys. The average number of pet services subscriptions increased slightly from 1.51 in April to 1.57 in August, while subscriptions to gym services and broadband both declined.

Streaming services

Streaming subscriptions ranked as the top choice for every age group except those aged 65 and older, in both the April and August surveys. The average number of subscriptions in this category even increased for those aged 45-54, rising from 2.98 in April to 3.16 in August.

Across the different income groups, subscriptions to streaming services ranged from a low average of 2.49 for those with an income of $75,000 – 99,999 per year, to a high of 3.31 for those making between $25,000 – 34,999 per year.

Magazines/newspapers/books

Respondents aged 65 or older led in the category of magazines/newspapers/book subscriptions in both surveys, though the average number of subscriptions for this group fell from 3.13 in April to 2.80 in August.

Those aged 55-64 were the second most likely to subscribe in this category, though the mean subscription rate also declined from 3.06 in April to 2.57 in August.

Notably, the mean subscription rate in this category rose from 1.71 in April to 2.20 in August for Gen-Z (age 18-25).

Millennials (age 35-44) were the least likely to subscribe in this category, with an average rate of 1.91 subscriptions.

Clothing/Cosmetics/Personal Care

The average number of subscriptions to clothing/cosmetics/personal care held fell from 2.3 to 2.21 in August 2022. Those making $75,000 – 99,999 per year have the highest average number of subscriptions in this category (3.03). This is also the highest-ranking specific category in this income group, and a notable increase from the average subscription rate of 1.57 in April 2022.

Pet services

Globally, people on average had 1.57 subscriptions to pet services in August 2022, with the lowest average found at the $15,000 - 24,999 income level (1.11).

In April 2022, those in the $100,000+ income bracket had the highest number of subscriptions to pet services, with an average of 2.23, though this fell to 1.56 in August.

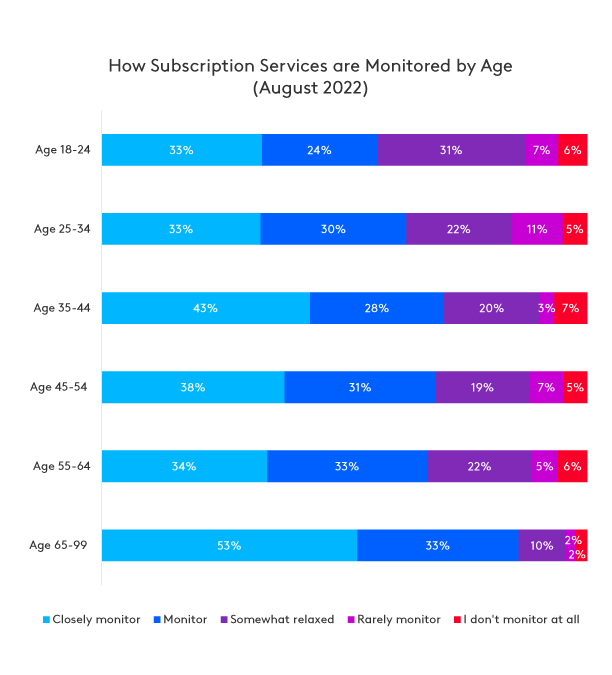

Older generations are more likely to monitor their expenditure and to claim benefits

The August 2022 survey shows that over half (53%) of those aged 65+ closely monitor their subscription expenditures, followed by 43% of the group aged 35-44. Thirty-three percent of those aged 18-24 and 25-34, 38% of those aged 45-54, and 34% of those aged 55-64 monitor subscription expenditures closely.

Older generations are also the most likely to claim refunds or benefits in three distinct categories. Eighty-one percent say they always claim refunds, while 71% always claim gift card benefits and 59% always claim any benefits or transfers from the government. The remaining results for these three categories decline in a linear pattern from the oldest cohort to the youngest. For example, with respect to gift cards, 65% of those aged 55-64 are likely to use them, compared to 53% (45-54), 51% (35-44), 38% (25-34), and 36% (18-25).

About this study

This research was conducted online using 1,000 respondents in the US sourced from the Kantar Profiles Audience Network.

All interviews were conducted as online self-completion in April 2022 and August 2022 and collected based on local census distributions for age, gender and income.

Each survey asked respondents about their use of subscription services across twelve categories (streaming services, entertainment services, magazines/newspapers/books, broadband, cellphone, insurance, utilities, gym, food/meal kits, clothing/cosmetics/personal care, pet services, other)

In this short report, Kantar focuses on key results for eleven specific subscription categories included in the survey and does not refer to results from an additional “other” category.