Grocery price inflation has slowed to 4.7% this month as retailers ramp up promotions ahead of Christmas. Take-home sales at the grocers grew by 3.2% over the four weeks to 2 November versus last year, with spending on deals specifically climbing by 9.4%. By comparison, spending on full priced goods rose by just 1.8%.

Christmas ads are hitting our screens and the race to the big day is on in the supermarket sector. Retailers are very alive to the financial struggles that some households are facing, not least ahead of this year’s Budget. They’re eager to show how they’re offering shoppers value for money, putting the emphasis on price cuts rather than multibuy offers. It’s not just the Grinch who’s looking for savings with just shy of 30% of consumer spending at the grocers on promoted items in October, a figure that we expect to go even higher as we get closer to Christmas.

Despite tightening belts, we are predicting a new sales record for retailer premium lines this year with the potential to hit more than £1 billion in December. It’s important to remember that shoppers often look for great value and quality, not just the cheapest product. At Christmas especially people want to treat themselves and throughout the cost of living crisis we’ve seen them turning to retailers’ premium own label lines to do that in a way that’s more affordable. Sales of these goods were worth £582 million in the latest month and they are likely to double as Christmas edges nearer, topping £1 billion in the month of December for the first time ever.

The grocers preparing for Black Friday fight with Amazon

Black Friday week could provide a significant sales boost for the grocers, particularly online. During this period last year, Amazon remained the destination retailer for general merchandise, while Tesco and Asda took second and third spot respectively in the battle for spend. Across the market, there was an average sales uplift of 114% with our data showing that electronics, beauty and toys had the biggest spike in sales versus a typical trading week in 2024.*

Online remains the fastest growing part of the grocery market and spending on home delivery rose by 11% this month, with every retailer who offers the service boosting sales. Online growth is primarily being driven by the already converted as existing shoppers continue to value the convenience of the format and make more orders. On average, households who use online grocery now buy three shops a month, making up a whopping 61% of their spending at the grocers.

Fastest growth for Ocado since 2021

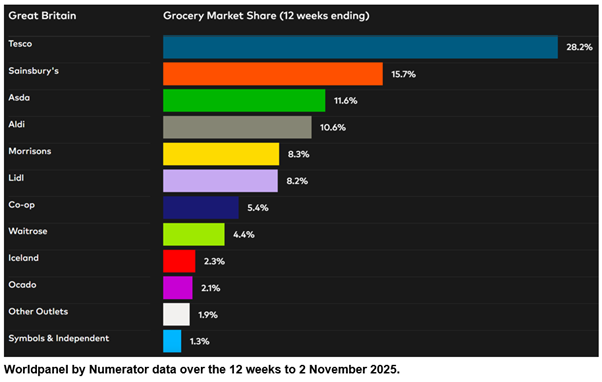

Benefiting from the popularity of online orders, Ocado posted a new record share for the 12 weeks to 2 November hitting 2.1%, as it remained the fastest growing grocer for the third month in a row. At 15.9%, Ocado registered its highest rate of sales growth in over four years since April 2021.

Tesco and Lidl both added half a percentage point of share to their market positions. Maintaining a run of double-digit growth from April, Lidl boosted sales by 10.8% over the 12 weeks to take its share to 8.2%. Tesco now accounts for 28.2% of the market as spending at Britain’s biggest grocer climbed by 5.9%. Sales growth of 5.2% took Sainsbury’s market share to 15.7%.

With 10.6% of the market, Aldi also won share and grew sales by 4.4%. Spending at Iceland increased by 4.9%, putting it ahead of the market rate. It has a share of 2.3%, up 0.1 percentage points on 2024.

Spending at Morrisons nudged up by 2.3% with a market share of 8.3%. Waitrose’s sales rose by 3.8% giving it a share of 4.4%. Convenience retailer Co-op now holds 5.4% of the market while Asda takes 11.6%. Looking across the wider high street, grocery sales at M&S over the 12 weeks increased at the fastest rate since June at 8.8% higher than one year ago.

*Source: Worldpanel Plus by Numerator, omnichannel data. Industries included are: appliances, beauty, consumer electronics, fashion, gifts, homeware, toiletries and toys during Black Friday week in 2024.

**Please note: with a higher proportion of clothing and general merchandise in its sales mix, M&S does not fall under the definition of ‘grocers’ using the Till Roll methodology on which the Worldpanel Grocery Market Share release is based. For this reason, a comparable market share number is not provided for M&S. The M&S growth number quoted in this update is for FMCG sales only, while the figures for grocers in the Grocery Market Share table cover total spending through supermarkets’ tills.