Imagine you are out for a Sunday afternoon stroll and decide to treat yourself. You pop into your local convenience store and pick up a small chocolate treat – a reward and a little energy boost, just what you needed.

Then you notice the price tag: £1.49. Still justifiable, you go ahead. But what if it was £2, or even £3? Would you still buy it or reject chocolate altogether, and buy a pack of biscuits instead?

That day may come sooner than expected. With raw cocoa prices reaching $12,639 [1] per tonne in late December 2024 and inflationary pressures expected to persist through 2025, manufacturers are finding their margins squeezed. Many are facing the challenge of having to push CPIs (Cost Price Increases) onto shoppers, which creates considerable anxiety for manufacturers, retailers, and shoppers alike, as increased prices can often lead to fewer products sold.

Inflation’s impact on chocolate

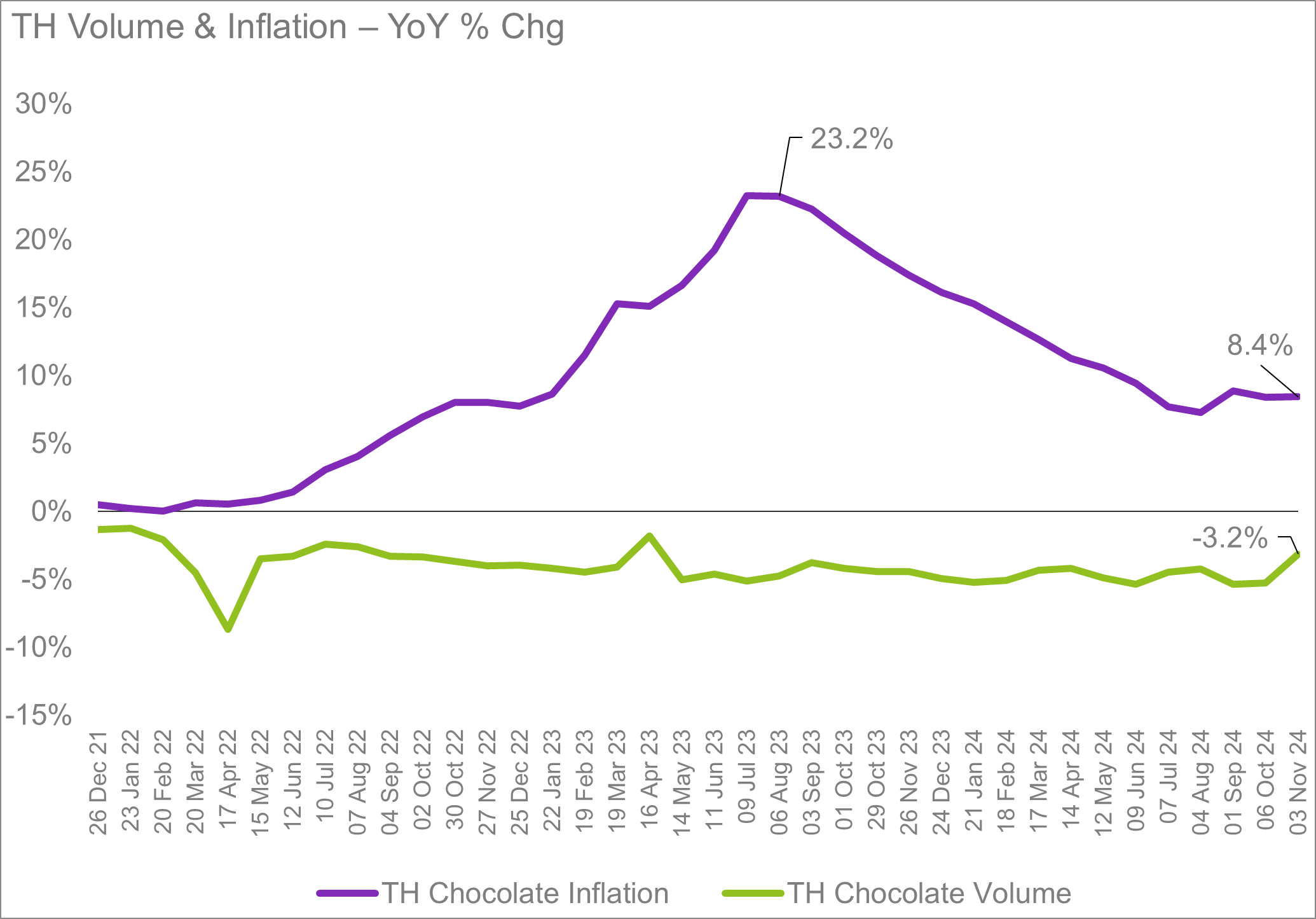

Over the past year, inflation in chocolate has been strong, far outweighing total grocery rates. Volumes, however, have not yet seen a corresponding decline. For now, chocolate confectionery continues to post healthy value growth rates – but there is a growing suspicion that a ceiling will come, when a chocolate bar treat becomes too expensive to be justifiable. Shoppers are already adapting and have begun voting with their baskets by switching away from treatsize (+24% £YoY) to seasonals (+13%) and multipack & snacksize (+9%) [2].

Coping Strategies: Shrinkflation and Skimpflation

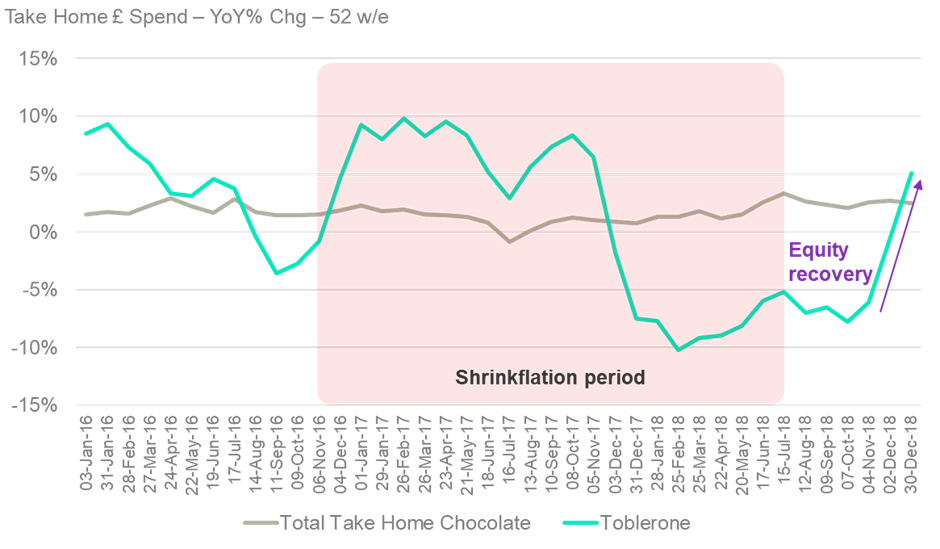

To mitigate price hikes, manufacturers can look to methods like shrinkflation – essentially a small reduction in volume in order to maintain a specific price point. The danger being even transparent attempts at this can backfire, as Toblerone infamously discovered November 2016. The damage wasn’t immediate, but by December 2017, sales had steadily declined by more than 7% year-over-year. By July 2018, the decision was reversed, and by December 2018, sales had spiked back into growth.

Skimpflation is a less well-known technique and far more subtle. This tactic involves adjusting the mixture of ingredients to reduce the proportion of the most expensive components, allowing margins to be preserved without implementing price increases. Imagine, then, that your chocolate bar is still £1.49, but it is no longer quite as chocolatey as before or now includes other ingredients like biscuit or fruit. With only 25% cocoa solids required to label a product as “milk chocolate,” these adjustments can go unnoticed unless shoppers consistently pay attention to ingredient lists. The innovation pipeline for 2025 is likely to feature more products of this nature. Cadbury appears to be setting the trend, having launched additional filled chocolate bars in March 2024. Looking ahead, it is anticipated that the announced partnership between Cadbury and Biscoff could contribute to this momentum, adding to the anticipation for 2025.

Navigating Risks

Both shrinkflation and skimpflation hold a risk of shopper backlash, eroding trust and engagement with your brand. With that in mind, here are three key tips for manufacturers pursuing these methods to mitigate price increases:

Be subtle: Ensuring product sizes remain comparable to competitors on the shelf can help maintain consistency in shopper perception. Companies can choose to either make adjustments subtly or proactively highlight a benefit resulting from shrinkflation—such as aligning with a specific calorie target.

Understand purchase considerations: How much volume comes from shoppers paying attention to £ per kg? This determines your risk.

Take advantage: See if you can hit a beneficial price point and use these changes to highlight positives– like a calorie reduction or price.

Alternative Approaches

If price increases are proving necessary, consider alternative approaches:

Justify price: Highlight what sets your brand apart from competitors, particularly if you need to move prices first.

Pack price architecture: Ensure your portfolio still caters to the range of packs/prices that shoppers require. A new, smaller tier may need to be introduced.

Diversify: if you can place investments elsewhere short-term, do-so – and wait for cocoa raw prices to fall off before pursuing chocolate growth.

Overall, chocolate manufacturers have already faced a challenging year and will see more of the same in 2025. Christmas, a time of indulgence, did look relatively positive in 2024 and I would expect the same for 2025.

[1] https://tradingeconomics.com/commodity/cocoa

[2] Kantar Worldpanel, Take Home Volume (Kgs) | 03 Nov 24 vs 05 Nov 23 | Actual | 52 w/e | (000 kg)

Chart 1: Kantar Worldpanel, Take Home Inflation 52 w/e 03 November 2024

Chart 2: Kantar Worldpanel, 52 w/e 30 December 2018, Take Home Chocolate