Take-home sales at the grocers increased by 2.5% over the four weeks to 1st December 2024 as shoppers get ready for Christmas, according to the latest data from Kantar. Supermarket sales are expected to continue growing, exceeding £13 billion over the four weeks of December for the first time ever.

Monday 23rd December is likely to be the single busiest day for the supermarkets this year, although there are clear signs that shoppers are already stocking up their cupboards. Sales of assorted sweet biscuits and biscuits for cheese both doubled in November compared with the month before, while 8% of us bought a Christmas pudding.

Many of us take the chance to treat ourselves at this time of year and retailers are rolling out seasonal product lines to help us celebrate in style. The proportion of spending on premium own label products reached 5% over the latest four weeks and we expect it to climb even higher in December to nearly 7%.

Outside of the food and drink aisles, retailers’ general merchandise lines are also predicted to get a boost. Spending on non-grocery items in the supermarkets leapt by 21% in December 2023 versus the monthly average for that year.*

Price cut deals push the level of promotion higher

The cost of an average Christmas dinner for four has risen to £32.57, up by 6.5%, largely driven by the price of turkey and Christmas vegetable staples. Wider grocery price inflation remains relatively stable at 2.6%, with grocers prioritising low pricing over multibuys. Sales on promotion reached 30% in November, the highest since Christmas last year. It’s retailer price cuts, often accessed through loyalty cards, that are really driving this. While multibuy promotions have stayed flat, spending on price cut offers has grown by 14%, worth £355 million more than last year. Shoppers are grabbing the chance to spend that little bit more than usual on Christmas specials, and champagne, wine and spirits saw the biggest levels of buying on deal.

Retailers line up for the Christmas run in

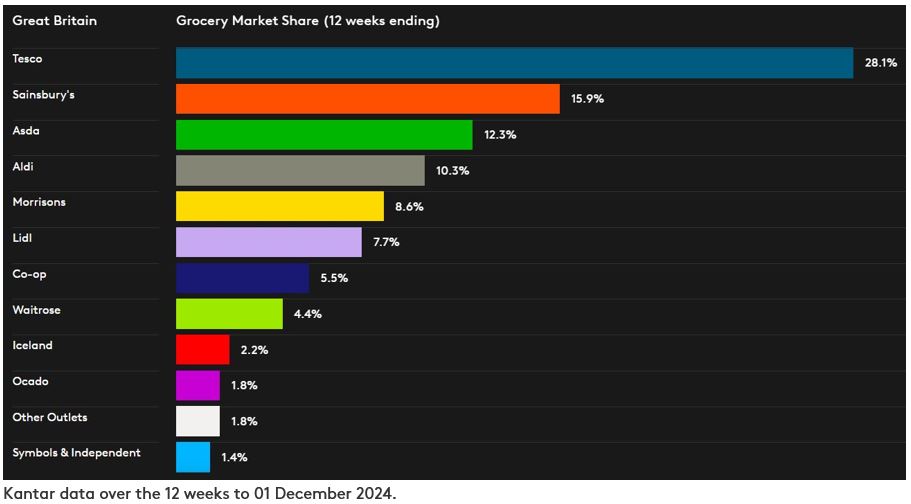

Britain’s largest grocer Tesco achieved its highest market share since December 2017 at 28.1%, up from 27.4% in 2023. Its sales grew by 5.2%. Sainsbury’s share increased by 0.3 percentage points to 15.9%, and spending through its tills was 4.7% higher than last year. The UK’s two biggest grocers now have a combined market share of 44%.

The number of different retailers we visit in the run up to Christmas is higher than at other times during the year, including wider high street brands like M&S. Just under one in three households, at 32%, bought food, drink and other groceries to have at home from M&S during the 12 weeks to 1 December and looking at grocery sales alone, spending at M&S rose by 10.4%.**

Online retailer Ocado boosted sales by 8.7% over the period, achieving a 1.8% share of the market. It outpaced the total online market which grew by 3.6%, with shoppers spending £4.2 billion on the channel overall across the 12 weeks.

Lidl was the fastest growing bricks-and-mortar grocer, with sales up by 6.6%. Its share climbed 0.3 percentage points to 7.7%. The retailer’s footfall stepped up by nearly 10% in comparison with a year ago.

Spending at Morrisons rose by 2.0%, and it now takes 8.6% of the market. Its average transaction value nudged up by 4.8% over the 12 weeks, helped by strong online sales. This was significantly ahead of the average growth in basket spend across the grocers as a whole, which edged 0.7% higher to £24.51 this period.

Waitrose grew slightly ahead of the market, with spending increasing by 2.6%. It maintains a 4.4% share. Spending at Aldi grew by 2.1%, and the retailer retained 10.3% of the market. Iceland also held its share of 2.2%, and Co-op’s portion of the market is now 5.5%. Asda has a 12.3% market share.

*Source: Kantar Worldpanel Plus physical and online monthly spend value for the appliances, arts & crafts, baby, beauty, electronics, DIY & garden, fashion, homeware, pet (not including food) and toys categories. The data compares the four weeks to 31 December 2023 to the monthly average in 2023. The sample size is 60,000 households in the United Kingdom. The grocers included in this data set are Tesco, Sainsbury’s, Asda, Morrisons, Aldi, Lidl, Co-op and Waitrose.

**Please note: with a higher proportion of clothing and general merchandise in its sales mix, M&S does not fall under the definition of ‘grocers’ using the Till Roll methodology on which the Kantar Grocery Market Share release is based. For this reason, a comparable market share number is not provided for M&S. The M&S growth number quoted in this update is for FMCG sales only, while the figures for grocers in the Grocery Market Share table cover total spending through supermarkets’ tills.

Notes to editors

Kantar monitors the take home grocery purchasing habits of 30,000 demographically representative households across Great Britain. This includes all expenditure through store tills at the grocers, excluding petrol and in-store concessions.

Retailer growth figures reported here relate to overall take-home sales, and so include the impact of store openings or closures. Like-for-like sales change is not measured or reported. Calculating like-for-like sales requires a detailed knowledge of store openings and extensions which is information held accurately only by individual retailers. For further information, please visit us at kantar.com/uki.