Take-home grocery sales grew by 4.4% over the four weeks to 18 May compared with last year, according to our new figures. In the same period, grocery price inflation also saw a marked rise to 4.1%, the highest level since February 2024.

This latest jump in grocery price inflation takes us into new territory for 2025. Households have been adapting their buying habits to manage budgets for some time, but we typically see changes in behaviour once inflation tips beyond the 3% to 4% point as people notice the impact on their wallets more. Own label lines are ones to watch, with premium own label, in particular, being the fastest growing part of the market since September 2023.

As consumers feel the pinch, many are continuing to seek out promotions to get the best value. The growth of spending on deals has carried on this month, increasing by 5.1% versus May last year. Trimming prices remains the most popular way for retailers to draw in customers, with 80% of promotional spending this period down to straightforward price cuts.

Consumers go alfresco in early heatwave

There were reasons to be cheerful, as Britons enjoyed the hottest ever start to May. We’ve been firing up the BBQs a bit earlier than last year, with chilled burgers flying off the shelves and sales growing by 27%. Shoppers didn’t forget the all-important sides, as sales of potato salad rocketed by 32% and coleslaw and prepared salads by 19% each. As the mercury rose, suncream sales also shot up to 36% as Brits made the most of the spring sun.

With the mid-year point approaching, we have been investigating what’s been trending in supermarket baskets*. It seems that consumers are shaping their diets around their lifestyle choices, with health, wellbeing and exercise apparently top of many people’s minds. Sports nutrition products have been the biggest winners. The number of these products bought has surged by 45% over the past five months versus the same time in 2024. Volume sales of cottage cheese, flatbreads and fresh prepared fruit have all been growing strongly too, up by 30%, 29% and 22% in each case.

Ocado leads retailer pack again

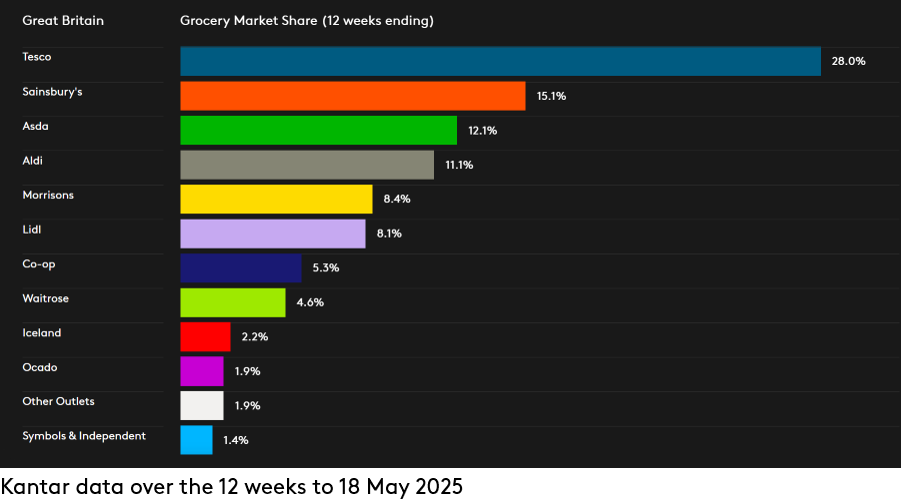

Ocado marks a full year as Britain’s fastest growing grocer, having held the position since June 2024. Over the 12 weeks to 18 May 2025, sales at the online retailer climbed by 14.9%.

It was a strong period for the discounters too, which achieved their strongest combined growth since January 2024 at 8.4%. Lidl reached a new share high of 8.1% with sales up by 10.9%. Compared with the same period last year, it brought 419,000 extra shoppers through its doors – the most of any retailer. Aldi’s hold of the market reached a record high at 11.1% with sales rising by 6.7%, its fastest growth rate since the start of last year.

Tesco boosted sales by 5.9% to increase its share by 0.4 percentage points. Britain’s largest grocer now has 28.0% of the market. Sales growth at Sainsbury’s accelerated by 4.7% giving it a 15.1% share.

Sales at Morrisons nudged up by 1.1% and it now holds 8.4% of the market. After Asda’s best performance since May last year, its share stands at 12.1%. Waitrose maintained a 4.6% share as sales grew by 4.0%. Spending through the tills at Iceland went up by 1.9%, bringing the frozen food specialist’s portion of the market to 2.2%.

The industry has been grappling with high-profile cybersecurity incidents of late. Despite these, spending on groceries at M&S** rose by 12.3%. Convenience retailer Co-op also faced challenges, but still increased sales by 0.6% to take 5.3% of the market.

*Year on year growth in packs over the 20w/e 18 May 2025 versus the same time period in 2024. Topp packaged categories greater than £25 million in sales

**Please note: with a higher proportion of clothing and general merchandise in its sales mix, M&S does not fall under the definition of ‘grocers’ using the Till Roll methodology on which the Kantar Grocery Market Share release is based. For this reason, a comparable market share number is not provided for M&S. The M&S growth number quoted in this update is for FMCG sales only, while the figures for grocers in the Grocery Market Share table cover total spending through supermarkets’ tills.